Ericsson’s second-quarter 2026 results point to several structural shifts underway across the telecom equipment market: operators remain disciplined on radio access network spending, software and services are becoming increasingly important to profitability, cost reductions are supporting higher infrastructure margins, and Ericsson is positioning AI-driven traffic growth as a catalyst for the next network investment cycle. The company reported SEK 52.7 billion in sales, down 1% organically, while adjusted gross margin increased to 48.4% and adjusted EBITA margin reached 13.1%.

The strongest trend emerged in Ericsson’s Cloud Software and Services business, where organic sales increased 5% with growth across all market areas. Adjusted gross margin reached 44.1%, while adjusted EBITA margin increased to 12.4% from 9.6% a year earlier. The rolling four-quarter EBITA margin reached 13.1%, a new high for the segment. The results indicate that Ericsson’s multi-year effort to improve software delivery economics and operating discipline is translating into materially higher profitability.

Ericsson’s Networks business remains the company’s financial engine despite a 4% organic sales decline during the quarter. Networks generated SEK 33.0 billion in sales and achieved an adjusted gross margin of 50.4%, up from 49.5% a year earlier, reflecting product mix improvements and cost reductions. The rolling four-quarter Networks gross margin remained above 50%, while the rolling four-quarter EBITA margin reached 20.2%. Ericsson expects Networks sales growth in Q3 to exceed three-year average seasonality and forecasts a Networks gross margin of 48% to 50%.

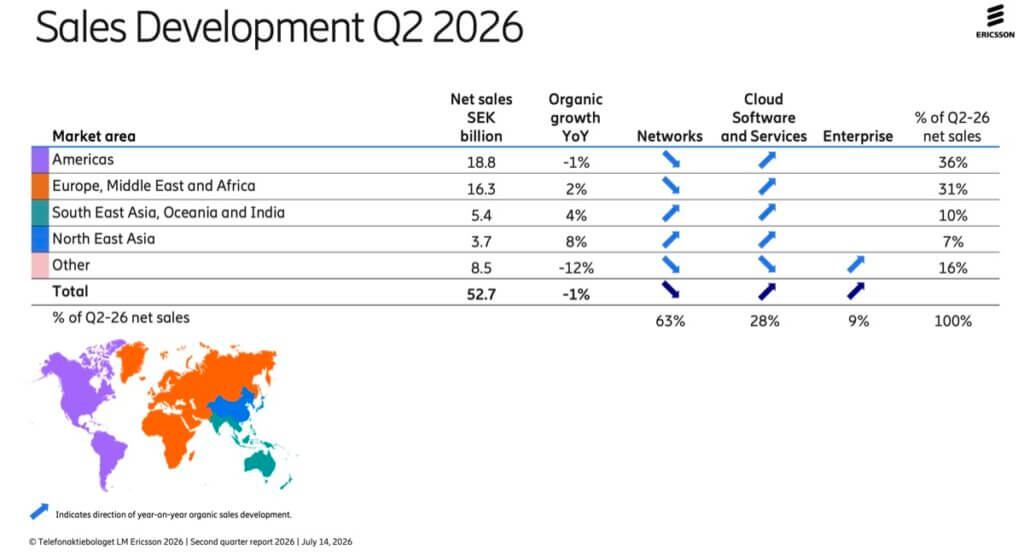

• Ericsson’s overall revenue base remains highly concentrated in mobile network infrastructure. Networks represented 63% of Q2 sales, Cloud Software and Services accounted for 28%, and Enterprise contributed 9%.

• The geographic composition of telecom investment continues to shift. Organic sales increased 8% in North East Asia, 4% in South East Asia, Oceania and India, and 2% across Europe, the Middle East and Africa. Sales declined 1% in the Americas.

• Margin expansion rather than top-line growth remains the dominant financial story. Ericsson increased adjusted gross margin to 48.4% despite lower revenue and SEK 1.8 billion of negative currency impact.

• Cloud Software and Services is becoming a more meaningful contributor to Ericsson’s profitability. The segment’s rolling four-quarter adjusted gross margin increased from 38% in Q3 2024 to approximately 44% in Q2 2026, while its rolling EBITA margin increased from 4% to 13%.

• Ericsson continues to generate substantial profitability from radio access network infrastructure. Networks maintained a rolling four-quarter gross margin above 50% and EBITA margin above 20%.

• Free cash flow before M&A declined to SEK 0.4 billion from SEK 2.6 billion a year earlier, primarily because of lower earnings and inventory accumulation ahead of planned Q3 deliveries.

• Ericsson ended the quarter with SEK 59.8 billion in net cash after returning SEK 8.2 billion to shareholders, including SEK 3.2 billion through share repurchases.

• Intellectual property licensing remains an important recurring revenue stream. Ericsson reported approximately SEK 13.5 billion in annual recurring licensing revenue and licensing agreements with all ten leading smartphone vendors.

• Ericsson expanded cellular IoT licensing into payment terminals and completed seventeen 4G and 5G licensing agreements with eleven Chinese automobile manufacturers through the Avanci licensing platform during the first half of 2026.

• The next major infrastructure cycle could increasingly center on AI-generated traffic and AI-native network operations. Ericsson explicitly identified the “next wave of AI-driven connectivity” as a longer-term growth opportunity while operators continue expanding 5G coverage and capacity.

• The underlying mobile traffic trajectory remains significant. Ericsson’s June 2026 Mobility Report data showed mobile network traffic increasing 22% between Q1 2025 and Q1 2026, while global 5G subscriptions exceeded 3 billion.

• A substantial infrastructure opportunity remains outside mainland China, where Ericsson estimates that half of the global population still lacks 5G coverage.

“Q2 demonstrates strong execution of operational and strategic priorities. Looking ahead, we are taking actions to help mitigate component cost inflation and are well positioned for the next wave of AI-driven connectivity,” Ericsson President and CEO Börje Ekholm said.

🌐 Analysis: Ericsson’s results illustrate a broader transition across the telecom equipment sector from maximizing 5G deployment volumes toward improving network economics, software profitability and automation. The strategic question for Ericsson and its competitors is whether AI workloads, increasing inference traffic, network APIs and AI-native RAN architectures can create a new investment cycle large enough to supplement the mature 5G radio market.

🌐 We’re tracking the latest developments in telecom networks, 5G, Open RAN, network automation and AI-driven connectivity. Follow our ongoing coverage at: https://convergedigest.com/category/5g/