Digital Realty is scaling aggressively to meet surging AI-driven infrastructure demand, reporting record leasing activity and expanding its global capacity pipeline as hyperscale and interconnection workloads accelerate.

The company posted Q1 2026 revenue of $1.6 billion, up 16% year-over-year, with Core FFO per share rising to $2.04. Total bookings reached $707 million at 100% share, including a record contribution from 0–1 MW and interconnection deployments, while backlog climbed to $1.8 billion, providing multi-year revenue visibility. Digital Realty also highlighted the largest hyperscale lease in its history during the quarter, underscoring the scale of AI-related demand.

“Digital Realty saw a further acceleration in data center demand and our growth trajectory in the first quarter, with record 0–1 megawatt plus interconnection leasing and the largest hyperscale lease in company history,” said CEO Andy Power. “We are swiftly advancing hyperscale AI-oriented capacity in the U.S., growing our connectivity-rich portfolio across key global markets, and broadening our capital base to prudently extend Digital Realty’s runway for growth.”

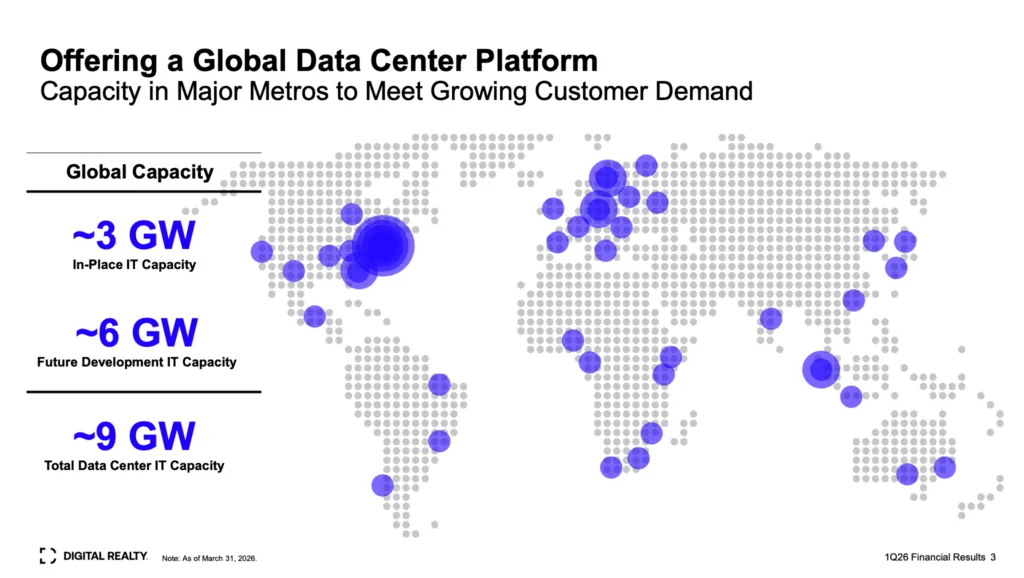

The company is investing heavily in future capacity, with a global pipeline now approaching ~9 GW of total IT load, including ~6 GW of development capacity. New land acquisitions in Atlanta and Portland, along with expansions in Europe and Asia, are designed to support large-scale AI deployments. Digital Realty raised its full-year Core FFO guidance to $8.00–$8.10 per share and increased its CapEx outlook to $3.5–$4.0 billion.

Key Infrastructure Trends

- Hyperscale AI demand is driving multi-gigawatt expansion cycles

Digital Realty now reports ~9 GW total global IT capacity (≈3 GW deployed + ≈6 GW future), reflecting rapid scaling to support AI training and inference workloads. - Shift toward large-scale (>100 MW) campus builds for AI clusters

Approximately 60% of future development capacity is in >100 MW blocks, signaling a structural move toward hyperscale AI campuses. - Interconnection and small-footprint deployments are surging alongside hyperscale

Record 0–1 MW plus interconnection bookings (+42% YoY) point to strong demand for AI ecosystems, edge inference, and network-dense deployments. - Backlog and leasing lag reflect long lead times for AI infrastructure delivery

A record $1.8B backlog with ~19-month lease commencement lag highlights supply constraints and extended build cycles. - Global “connected campus” strategy expanding across key metros

ServiceFabric now spans 700+ data centers across nearly 40 metros, emphasizing distributed, connectivity-rich architectures. - Land banking for power-constrained AI growth is accelerating

Over 1 GW of additional land capacity was secured in Q1, reflecting the strategic importance of power availability. - Emerging markets becoming strategic connectivity hubs

Expansion into Bulgaria, Italy, and Malaysia highlights demand for globally distributed AI and cloud infrastructure tied to subsea routes. - Hybrid demand mix: hyperscale capacity + enterprise ecosystems

Large deals (>1 MW) dominate, but rising smaller deployments indicate a dual market of AI training and enterprise/edge connectivity. - Private capital and balance sheet diversification fueling build-out

Joint ventures and capital partnerships are enabling large-scale expansion while maintaining balance sheet discipline. - Pricing power remains intact amid supply-demand imbalance

Renewal rates increased ~5% (cash), reflecting tight supply in AI-ready and connectivity-rich data center environments.

🌐 Analysis

Digital Realty’s results reinforce a critical shift in data center architecture: the transition from traditional colocation to AI-scale infrastructure platforms. The emergence of >100 MW deployment blocks—and the concentration of future capacity in these large footprints—mirrors hyperscaler demand for “AI factories” capable of supporting dense GPU clusters, high-speed fabrics, and massive power envelopes.

At the same time, the sharp rise in interconnection and sub-megawatt deployments highlights a parallel trend: AI is not only centralized but also increasingly distributed. Training clusters require proximity to dense connectivity ecosystems, while inference workloads are expanding toward edge and enterprise environments. This dual demand model is reshaping facility design, favoring campuses that combine hyperscale capacity with rich interconnection fabrics.

The nearly two-year lag between lease signing and delivery further underscores a tightening supply environment. Power constraints, permitting timelines, and the complexity of building AI-ready facilities are extending deployment cycles, reinforcing the value of existing inventory and driving pricing strength.

Looking ahead, Digital Realty’s aggressive land banking and global expansion suggest that control of power, land, and connectivity ecosystems—not just real estate—will define competitive positioning in the AI infrastructure era. The company’s strategy aligns closely with hyperscaler buildouts and the broader industry shift toward multi-gigawatt, globally distributed AI infrastructure platforms.

🌐 We’re tracking the latest developments in data center infrastructure and AI networking. Follow ongoing coverage at convergedigest.com/category/data-centers