A simplified Vodafone aims to leverage cross-border scale across Europe and Africa to drive operational efficiency, converged services, and long-term cash flow growth

Vodafone entered FY27 with a significantly reshaped portfolio, a new operating model, and a strategy centered on operational scale, AI-driven efficiency, converged connectivity, and selective growth markets. Following the disposals of Vodafone Spain and Vodafone Italy, the company now positions itself as a more focused European and African operator with stronger market positions and simplified operations. Vodafone describes the strategy as “Simpler, Stronger, Growing,” with management targeting double-digit medium-term adjusted free cash flow growth and further EBITDAaL acceleration in FY27.

The FY26 results showed mixed operational momentum across regions. Group service revenue increased 5.4% organically, while adjusted EBITDAaL rose 4.5% to €11.4 billion. Europe returned to marginal growth, Africa continued double-digit expansion, and Vodafone Business sustained digital services momentum. Germany remained the primary turnaround challenge, with service revenue declining 0.2% due to competitive mobile ARPU pressure and the lingering impact of Germany’s MDU TV law changes. Meanwhile, the UK merger with Three became the centerpiece of Vodafone’s European consolidation strategy, creating the country’s largest spectrum holder and positioning the combined operator to accelerate 5G Standalone deployment and convergence offerings.

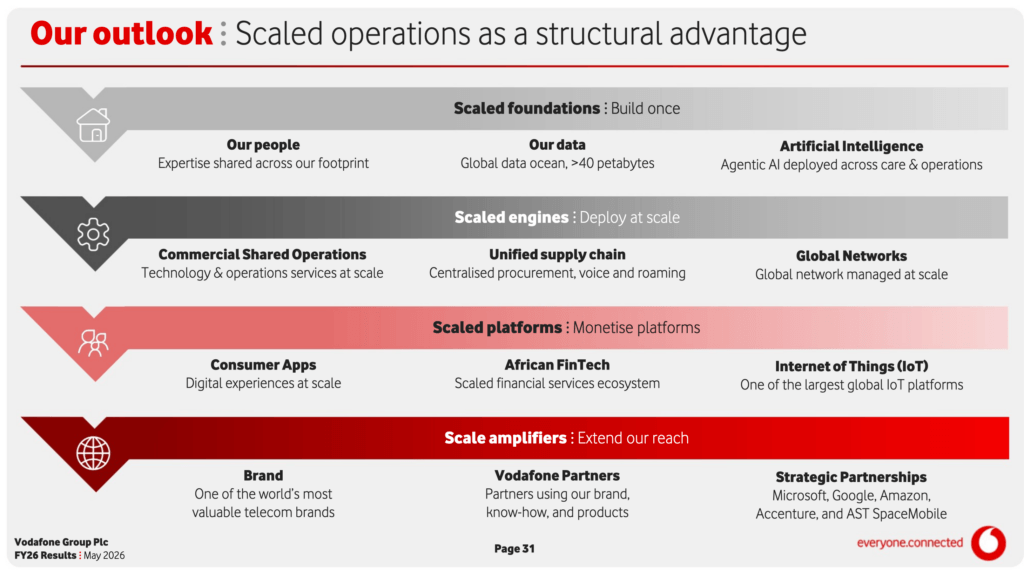

Vodafone’s “new chapter” strategy relies heavily on using scale as a shared operating system across Europe and Africa. The company highlighted centralized procurement, shared network operations, AI-enabled customer care, and cross-market automation as structural advantages. Vodafone claims its centralized operations now support more than 244 million IoT connections, 103 million financial services users, and 5 million business customers across Europe and Africa. AI increasingly sits at the center of this model. Vodafone reported GenAI deployment across customer service, procurement, software development, and network automation, including AI-enabled “Ask Once” customer care, autonomous procurement, and AI-powered network optimization.

Geographic Outlook

Germany

Vodafone’s largest EBITDA contributor remains a turnaround story. Germany represented 37% of Group EBITDAaL in FY26, but revenue growth remained under pressure from mobile competition, TV subscriber declines, and broadband market intensity. Vodafone’s strategy focuses on improving customer experience, expanding hybrid fiber-cable density, monetizing converged services, and scaling AI-based care systems such as SuperTOBi and “Ask Once.”

UK

The UK now represents Vodafone’s clearest scale thesis. VodafoneThree combines the UK’s largest spectrum position with broad consumer and enterprise reach. Vodafone plans approximately €1.6 billion in FY27 capital additions to integrate the networks and expand 5G Standalone coverage nationwide. The company expects network integration synergies, converged mobile-broadband bundles, and premium network monetization to drive long-term returns.

Other Europe

Markets including Portugal, Greece, and Romania showed relatively stable growth, though ARPU pressure persists in Southern Europe. Vodafone completed the Telekom Romania acquisition integration and continues to push digital business services and pricing adjustments to stabilize profitability.

Africa

Africa increasingly represents Vodafone’s structural growth engine. The region delivered 12.9% service revenue growth in FY26, fueled by mobile data usage, fintech expansion, and pricing improvements. Vodafone’s African operations now span nearly 50,000 mobile sites, while M-Pesa and Vodafone Cash continue to expand financial services penetration. The company sees Africa as both a telecom and fintech growth platform, targeting 130 million financial services users by FY30.

Vodafone Business

Vodafone Business increasingly acts as the diversification layer above connectivity. Digital services revenue grew 14.2% in FY26, with strong growth in SaaS, SDN, cloud, cybersecurity, and sovereign cloud services. Vodafone’s partnerships with AWS, Google, Microsoft, and Accenture form a core element of its enterprise strategy, especially around sovereign cloud, AI-enabled services, and security.

Key points

- Vodafone targets double-digit medium-term adjusted free cash flow growth.

- FY26 Group service revenue increased 5.4% organically.

- Africa delivered 12.9% service revenue growth and remains Vodafone’s highest-growth geography.

- VodafoneThree UK becomes Vodafone’s primary European scale and consolidation play.

- Germany remains the key operational turnaround challenge.

- Vodafone Business digital services revenue increased 14.2% in FY26.

- AI and shared operations now underpin Vodafone’s efficiency strategy.

- Vodafone plans approximately €1.6 billion in FY27 UK network investment.

- Capital intensity remained stable at approximately 18% of revenue.

- Vodafone reduced net debt by approximately €8 billion over three years.

Margherita Della Valle, Vodafone Group Chief Executive, said the company now operates with “a simpler Vodafone, with a clear operating model,” adding that Vodafone sees “attractive opportunities in Europe, Africa and B2B” while leveraging “scaled operations, building once and deploying at scale.”

| Vodafone’s New Chapter Strategy | |

|---|---|

| Strategic Theme | “Simpler, Stronger, Growing” strategy focused on operational simplification, scale efficiencies, AI-enabled automation, convergence, enterprise services, and long-term free cash flow growth. |

| Core Geographic Footprint | 9 European markets and 8 African markets serving approximately 350 million mobile customers combined across Vodafone and Vodacom operations. |

| FY26 Group Performance | Group service revenue growth: +5.4% organic. Adjusted EBITDAaL: €11.4 billion (+4.5%). Adjusted free cash flow: €2.6 billion. |

| Medium-Term Financial Ambition | Targeting double-digit organic adjusted free cash flow growth with accelerating EBITDAaL expansion and stable capital intensity. |

| Scale Strategy | Centralized procurement, shared operations, AI-enabled automation, common platforms, and cross-border network operations designed to create structural cost advantages across Europe and Africa. |

| AI & Automation | GenAI deployed across customer care, procurement, software development, HR, and network operations. Key initiatives include: • “Ask Once” AI-assisted customer care • SuperTOBi GenAI virtual assistant • AI-powered customer value management • Autonomous procurement portal • Zero-touch network operations |

| Germany Strategy | Vodafone’s largest EBITDA market (37% of Group EBITDAaL). Focus areas: • Customer experience improvements • AI-powered service automation • Gigabit broadband expansion • Fiber partnerships through OXG • Converged mobile + broadband offers Challenge: mobile ARPU pressure and lingering MDU TV law impacts. |

| UK Strategy | VodafoneThree merger creates the UK’s largest spectrum holder and a major European consolidation play. FY27 planned investment: approximately €1.6 billion. Priorities: • Nationwide 5G Standalone integration • Convergence and family bundles • Network monetization • Multi-brand customer segmentation |

| Africa Growth Engine | Africa service revenue growth: +12.9% in FY26. Structural growth drivers: • Mobile data demand • Smartphone adoption • Financial services expansion • Population growth Vodafone targets 130 million financial services users by FY30. |

| Fintech & Mobile Money | 103 million financial services users across Africa. M-Pesa and Vodafone Cash generated strong double-digit growth. Financial services revenue reached approximately €2 billion in FY26. |

| Vodafone Business | Business digital services revenue growth: +14.2% in FY26. Strategic areas: • Sovereign cloud • SDN services • Cybersecurity • IoT connectivity • AI-enabled enterprise services • 5G slicing |

| Technology Scale | • 158,000 mobile sites across Europe and Africa • 84 million marketable gigabit broadband households • 70 subsea cable investments/co-ownerships • 1 million kilometers of terrestrial fiber • Connectivity reach across 180 countries |

| Satellite Strategy | Vodafone pursuing direct-to-mobile and satellite connectivity through partnerships with AST SpaceMobile and Satellite Connect Europe. Goal: ubiquitous connectivity and coverage extension across 20+ markets. |

| Customer Experience Focus | Vodafone now leads or co-leads Net Promoter Scores in 11 markets. Convergence, AI customer care, and network reliability positioned as primary customer retention drivers. |

| CAPEX Outlook | Group capital intensity remains stable near 18% of revenue. Investment priorities include: • UK network integration • German broadband infrastructure • 5G Standalone deployment • AI-enabled operations • African network expansion |

| Efficiency Program | Vodafone exceeded its target of 10,000 role reductions, reaching approximately 11,000 by FY26. Company targets approximately €1 billion net European opex reduction opportunity between FY27–FY30. |

| Capital Structure | Net debt reduced by approximately €8 billion over three years. FY26 leverage: 2.2x net debt / EBITDAaL. Vodafone targets the lower half of its 2.25x–2.75x leverage range. |

| Strategic Thesis | Vodafone believes its competitive advantage comes from combining geographic scale, AI-driven operational leverage, converged connectivity, enterprise platforms, fintech ecosystems, and shared infrastructure across Europe and Africa. |

🌐 Analysis: Vodafone’s strategy marks one of the clearest examples of a European telecom operator attempting to reposition scale as a software and operational advantage rather than simply a coverage metric. Historically, European telecom consolidation arguments focused on spectrum efficiency and pricing power. Vodafone now frames scale around AI deployment, procurement leverage, shared software platforms, and cross-market operational reuse. The UK merger becomes the company’s flagship proof point for this thesis.

ARPU trends remain the core stress point. Germany still faces competitive mobile pricing pressure, Portugal shows ongoing ARPU weakness, and mature European telecom markets remain structurally difficult for premium pricing. Vodafone’s response centers on convergence, customer experience, AI-enabled retention, and enterprise digital services rather than pure connectivity pricing. The company increasingly appears to view B2B, fintech, sovereign cloud, IoT, and security services as the primary engines for long-term margin expansion.

CAPEX discipline also sits at the center of the strategy. Vodafone repeatedly emphasized “stable capital intensity” while selectively increasing investment in high-return assets such as UK 5G integration, gigabit broadband, AI automation, and African mobile-financial infrastructure. The company’s long-term success may depend less on absolute scale and more on whether it can convert that scale into sustainable operating leverage faster than rivals such as Deutsche Telekom, Orange, Telefónica, and Liberty Global.