Alphabet reported a surge in AI-driven growth across its cloud, infrastructure, and consumer platforms in Q1 2026, with Google Cloud emerging as the central engine for enterprise AI demand. Total revenue reached $109.9 billion, up 22% year-over-year, while operating income rose 30% to $39.7 billion, reflecting expanding margins and scaling efficiency across AI investments.

Google Cloud revenue jumped 63% to $20.0 billion, with operating income tripling to $6.6 billion and margins expanding to nearly 33%. The growth reflects accelerating enterprise adoption of AI infrastructure and services, including Google Cloud Platform (GCP) and Gemini-based AI solutions. Notably, Alphabet reported a cloud backlog exceeding $460 billion and rapid uptake of Gemini Enterprise, with paid monthly active users up 40% quarter-over-quarter. At the infrastructure layer, first-party AI models are now processing over 16 billion tokens per minute via API usage, up 60% sequentially, underscoring the scale of compute demand being absorbed by Google’s AI stack .

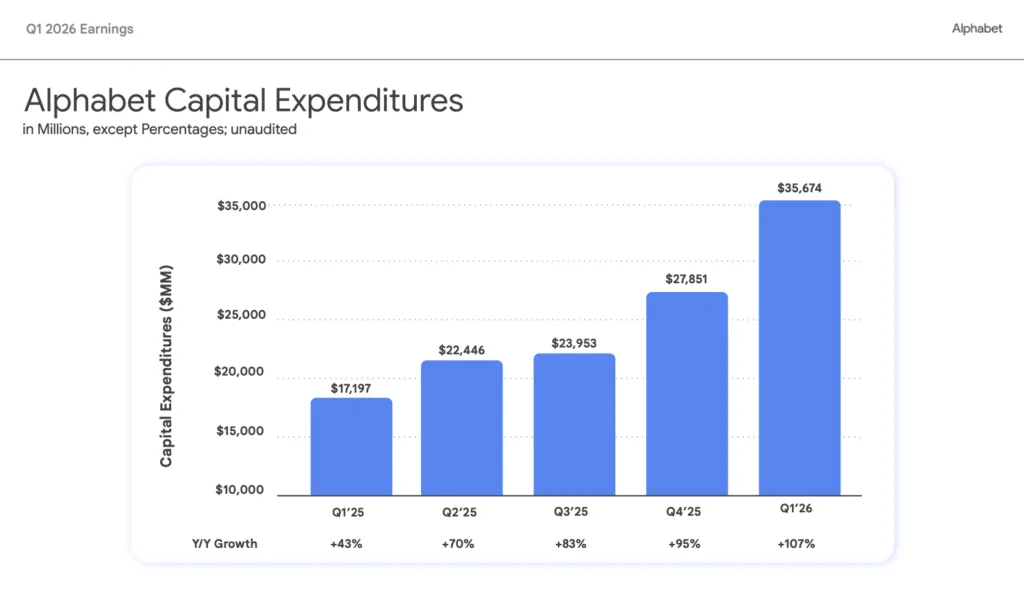

Across the broader business, AI integration continues to drive performance in core services. Google Search revenue rose 19% as AI-generated experiences increased query volume, while subscriptions—including YouTube and Google One—reached 350 million paid users. Capital expenditures remain elevated, with Q1 spending at $35.7 billion, highlighting ongoing investment in data center infrastructure, custom silicon, and networking capacity to support AI workloads. Alphabet also issued $31.1 billion in debt during the quarter, signaling continued aggressive scaling of its AI infrastructure footprint.

• Google Cloud revenue: $20.0B (+63% YoY); operating income: $6.6B; margin: ~33%

• Cloud backlog exceeds $460B, reflecting long-term enterprise AI demand

• AI infrastructure scale: 16B+ tokens per minute processed (+60% QoQ)

• Gemini Enterprise MAUs up 40% QoQ; strong enterprise AI adoption

• CapEx: $35.7B in Q1, up sharply to support AI data centers and compute

• Google Services revenue: $89.6B (+16% YoY), led by Search and subscriptions

• Paid subscriptions: ~350M across YouTube, Google One, and other services

• Waymo surpasses 500,000 fully autonomous rides per week

• Net income: $62.6B (+81% YoY); EPS: $5.11 (+82%)

“2026 is off to a terrific start. Our AI investments and full stack approach are lighting up every part of the business… Google Cloud revenues grew 63%… and our first-party models are now processing more than 16 billion tokens per minute via direct API use by our customers.” — Sundar Pichai

Addendum: Infrastructure, AI, and Silicon Notes from Alphabet’s Q1 2026 Call

• Alphabet said its AI infrastructure strategy centers on a vertically optimized stack spanning custom TPUs, Axion CPUs, NVIDIA GPUs, Gemini models, cloud platforms, enterprise agents, and security services.

• Google Cloud will offer NVIDIA Vera Rubin NVL72 instances, adding to existing Blackwell- and Hopper-based GPU offerings.

• Alphabet introduced eighth-generation TPUs at Cloud Next, with separate designs for training and inference. TPU 8t targets high-performance training with 3x the processing power of Ironwood and 2x the performance. TPU 8i targets low-latency inference with 80% better performance per dollar than the prior generation.

• Google plans to deliver TPUs directly to select customers for deployment in their own data centers, expanding beyond Google-operated cloud infrastructure. Initial revenue from those agreements should begin later in 2026, with most revenue expected in 2027.

• Management said TPU demand now extends beyond AI labs into capital markets firms and high-performance computing applications.

• CFO Anat Ashkenazi said Q1 CapEx reached $35.7 billion, with the overwhelming majority directed toward technical infrastructure. About 60% went to servers and 40% to data centers and networking equipment.

• Alphabet raised its full-year 2026 CapEx outlook to $180 billion–$190 billion and said 2027 CapEx should increase significantly as internal and external AI compute demand remains constrained.

• Sundar Pichai said Google Cloud revenue would have been higher if the company had enough compute capacity to meet demand.

• Google Cloud’s AI solutions became its primary growth driver for the first time. Revenue from products built on Google’s GenAI models grew nearly 800% year-over-year.

• Over the past 12 months, 330 Google Cloud customers each processed more than 1 trillion tokens, while 35 customers crossed the 10 trillion-token mark.

• Google introduced Gemini Enterprise Agent Platform and Agentic Data Cloud, including Cross-Cloud Lakehouse, Knowledge Catalog, and Deep Research agents.

• BigQuery adoption tied to AI agents accelerated, with Gemini-powered workflows in BigQuery growing more than 30x year-over-year.

• Google said AI response costs in Search fell by more than 30% after upgrading AI Overviews and AI Mode to Gemini 3, citing hardware and engineering improvements.

• Search latency dropped more than 35% over the past five years, even as Google added AI features to the results page.

• Google framed the Wiz acquisition as part of its AI security strategy, adding Gemini-powered agents for threat detection, continuous red teaming, and automated remediation.

• Management emphasized ROIC as the framework for allocating constrained compute capacity among model training, Search, YouTube, Google Cloud, enterprise AI, and selective TPU hardware sales.

• Google said its scale and full-stack control help it manage a constrained supply chain, deepen supplier partnerships, and improve economies of scale across AI infrastructure.

• Higher CapEx will pressure future P&L through depreciation, energy costs, and data center operations expenses, even as Google targets efficiency gains across technical infrastructure and internal AI-assisted engineering workflows.

🌐 Analysis: Alphabet’s results reinforce a clear industry shift toward vertically integrated AI infrastructure, where hyperscalers control the full stack—from custom silicon and data centers to models and APIs. The scale of Google’s token processing and backlog positions it alongside competitors like Microsoft Azure and Amazon Web Services in a race defined by compute capacity, networking bandwidth, and AI model monetization. Rising CapEx signals continued pressure on supply chains for GPUs, optical interconnects, and power infrastructure as AI workloads expand.