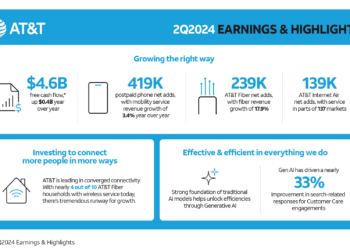

AT&T Inc. reported first-quarter 2026 results showing accelerating momentum in its “converged connectivity” strategy, as fiber broadband and 5G wireless increasingly operate as a unified infrastructure platform. The company posted $31.5 billion in revenue, up 2.9% year over year, driven by growth in its Advanced Connectivity segment, where bundled fiber and wireless adoption continues to scale. Nearly 45% of advanced home internet subscribers now also take AT&T wireless, marking the fastest organic growth in convergence rates in the company’s history.

The results highlight a broader infrastructure shift underway: operators are moving beyond standalone access networks toward tightly integrated fiber and wireless architectures. AT&T added 584,000 total internet subscribers in the quarter, evenly split between fiber (292,000) and fixed wireless (292,000), while extending its fiber footprint to more than 37 million locations—boosted by the acquisition of fiber assets from Lumen Technologies. The company remains on track to surpass 40 million fiber locations by the end of 2026 and reach over 60 million by 2030, underscoring the scale of its long-term infrastructure buildout.

Capital intensity remains elevated as AT&T accelerates fiber deployment and network upgrades, with $5.1 billion in capital investment during the quarter and full-year expectations of $23–24 billion. At the same time, legacy copper infrastructure continues to be decommissioned, with legacy revenues declining more than 25% year over year. This transition reflects a structural pivot toward high-capacity, IP-based networks optimized for multi-gig broadband, fixed wireless access, and mobile services—forming the foundation for next-generation applications, including AI-driven services and distributed cloud connectivity.

- Converged connectivity gaining traction: ~45% of fiber customers also subscribe to AT&T wireless

- 584,000 internet net adds: 292,000 fiber + 292,000 fixed wireless

- 294,000 postpaid phone net adds; churn at 0.89%

- Fiber footprint reaches 37M+ locations; targeting 60M+ by 2030

- $5.1B quarterly capital investment; $23–24B expected for full-year 2026

- Advanced Connectivity revenue: $22.9B (+3.6% YoY); operating income up 14.8%

- Legacy copper revenues down 25%+ as network decommissioning accelerates

- Free cash flow: $2.5B; adjusted EBITDA: $11.8B

“We’re uniquely positioned to deliver more of what customers want — fiber and 5G all from one provider on the nation’s largest advanced converged network,” said John Stankey, Chairman and CEO of AT&T.

Addendum from AT&T’s Q1 2026 investor call:

- AT&T framed “open” network architecture as a core infrastructure theme for the rest of the decade. John Stankey said this includes more open wireless network design to improve supply-chain flexibility and economics, plus a major re-architecture of the company’s core routing infrastructure into a flatter, software-driven network that can expose APIs for customers and partners.

- Management tied that network redesign directly to AI-era requirements. Stankey said AT&T is building for symmetrical capacity, ultra-low latency, and session control across multiple access technologies under sustained load, arguing that future AI-enabled applications will require more than raw download speed.

- The company described OneConnect less as a near-term volume driver and more as a platform for future offer design. AT&T is initially targeting BYOD customers and smaller accounts, especially one- and two-line households that it believes can grow over time into larger, higher-lifetime-value converged relationships.

- AT&T signaled a gradual shift in wireless packaging away from an overreliance on device subsidies and toward service-led value propositions. Management said OneConnect is a foundational step in rebalancing the portfolio so customers focus more on network value and bundled connectivity rather than handset promotions alone.

- In business services, management highlighted an important inflection: Advanced Connectivity business service revenue was flat year over year for the first time, as growth in fiber and 5G offset declines in transitional services such as VPN. AT&T said it now expects business service revenue within Advanced Connectivity to remain stable in the near term and grow at a low-single-digit CAGR through 2028.

- On the Lumen assets, AT&T said the near-term priority is operational buildout rather than immediate profit contribution. The company is investing to scale engineering, construction, service delivery, and go-to-market coverage in the acquired metros, with management expecting performance in those regions to improve month by month as 2026 progresses.

- Management pointed to the EchoStar spectrum transaction as both a performance and capital-efficiency play. Stankey said AT&T is already seeing better network perception in markets where leased spectrum has been deployed, while also using the added capacity to expand Internet Air and improve its ability to pursue larger enterprise and multi-location broadband bids.

- AT&T’s comments on fixed wireless were more nuanced than the press release. The company sees Internet Air as both a standalone product for selected customer segments and as a strategic bridge into future fiber markets, where AT&T can establish a customer relationship first and later migrate that household to fiber.

- On satellite, AT&T emphasized partnership and integration over disruption. Stankey said the company expects direct-to-device satellite services to become important, but argued that terrestrial fiber and wireless remain the foundational assets for performance, economics, and service control. He also indicated AT&T would prefer wholesale relationships with multiple LEO providers rather than depend on a single constellation.

- The copper retirement program emerged as a major cost and infrastructure story. AT&T said more than 30% of its wire centers are now on a definitive shutdown schedule, and management expects additional activity in the coming months. Stankey described the FCC’s recent direction as a strong roadmap for accelerating the retirement of aging, power-hungry, less secure copper infrastructure.

- Management also gave more color on the margin and cash flow cadence for the rest of the year. Pascal Desroches said EBITDA and service revenue growth should improve in Q2 and continue building through the year, helped by pricing actions, ongoing cost reductions, and improving operating performance from the acquired Lumen footprint.

- AT&T suggested the next phase of fiber monetization will come from moving beyond early penetration wins. Stankey said getting from 0% to 40% fiber penetration is a different play than moving from 40% to 50%, with the latter likely requiring more value-oriented offers and potentially some ARPU dilution that management still considers economically rational.

- On broadband competition, AT&T downplayed the long-term threat from satellite in areas where it has fiber. Management repeatedly returned to the view that fiber offers the best performance and the lowest marginal cost per bit, which it sees as the strongest position for defending share and driving converged growth over time.