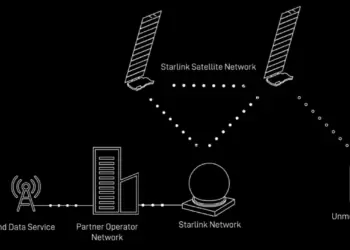

US Mobile is preparing to bundle Starlink residential broadband with its multi-network wireless offering, shifting the narrative from direct-to-device satellite mobility to a combined home internet plus cellular service model. The offer pairs Starlink’s LEO-based fixed broadband with US Mobile’s MVNO access across all three major U.S. networks—Verizon, AT&T, and T-Mobile—under a single subscription reportedly priced below $50 per month.

The bundled model positions US Mobile as an aggregator of access networks rather than a facilities-based provider, combining fixed satellite broadband with nationwide cellular coverage. Starlink continues to operate as a standalone residential service, typically priced around $120 per month in the U.S., but US Mobile’s approach integrates that offering into a broader connectivity package. Internally, US Mobile markets its network options as “Warp” (Verizon), “Dark Star” (AT&T), and “Light Speed” (T-Mobile), enabling users to select or switch among underlying carrier infrastructure depending on coverage and performance.

The announcement follows the expiration of exclusivity dynamics around Starlink’s U.S. mobility partnerships, most notably with T-Mobile, opening the door for additional service providers to incorporate Starlink into their portfolios. Rather than competing on infrastructure, US Mobile is leveraging wholesale access and service integration to introduce a bundled pricing construct that contrasts with traditional standalone broadband and mobile plans.

US Mobile background

Founded in 2015 and headquartered in New York, US Mobile operates as a mobile virtual network operator (MVNO), purchasing capacity from major U.S. carriers and delivering it through software-defined service plans. The company has focused on flexible pricing, eSIM-based activation, and pooled or customizable data plans for consumers and small businesses.

US Mobile’s strategy emphasizes aggregation across multiple networks rather than dependence on a single host carrier. Its platform enables dynamic selection between Verizon, AT&T, and T-Mobile infrastructure, a capability that becomes more differentiated when paired with satellite broadband. By integrating Starlink into its portfolio, US Mobile extends its reach into fixed broadband without deploying physical access infrastructure.

Starlink in the broadband and mobile ecosystem

SpaceX’s Starlink has primarily scaled as a residential and enterprise broadband service, with millions of subscribers globally, particularly in rural and underserved regions. While the company is actively developing direct-to-device (D2D) capabilities with partners such as T-Mobile, most commercial deployments today remain focused on fixed wireless access via user terminals.

Globally, Starlink partnerships with mobile operators—such as KDDI, Optus, and Rogers Communications—have centered on extending coverage through satellite backhaul or future D2D services. The US Mobile announcement differs in that it bundles existing residential broadband service with cellular access, rather than introducing new satellite-native mobile capabilities.

• US Mobile is bundling Starlink residential broadband with nationwide cellular service across Verizon, AT&T, and T-Mobile

• The combined offering is reportedly priced under $50/month, significantly below standalone Starlink pricing (~$120/month)

• The model aggregates fixed satellite broadband and mobile connectivity into a single subscription

• US Mobile operates as an MVNO with multi-network access (“Warp,” “Dark Star,” “Light Speed”)

• Starlink remains primarily a fixed broadband service today, with D2D mobile capabilities still emerging

• The move reflects a service-layer disruption rather than new infrastructure deployment

“By integrating satellite connectivity into our platform, we’re ensuring our customers stay connected wherever they are—without relying solely on traditional cellular infrastructure,” the company said in its announcement.

🌐 Analysis: This approach reframes competition in U.S. telecom from infrastructure ownership to service aggregation. By combining Starlink broadband with multi-network cellular access, US Mobile highlights a potential path for MVNOs to challenge incumbents on pricing and packaging. At the same time, incumbent carriers continue to invest heavily in satellite partnerships—such as AST SpaceMobile backing from AT&T and ongoing work by T-Mobile with Starlink—suggesting that hybrid terrestrial-satellite strategies will evolve across both retail bundles and deeper network integration.