Microsoft posted double-digit growth in its fiscal Q2 2026 quarter ended Dec. 31, 2025, as cloud and AI demand lifted revenue to $81.3 billion (+17% YoY) and operating income to $38.3 billion (+21%). Intelligent Cloud revenue rose to $32.9 billion (+29%), driven by Azure and other cloud services growth of 39% (38% constant currency), while Microsoft Cloud revenue reached $51.5 billion (+26%, 24% constant currency).

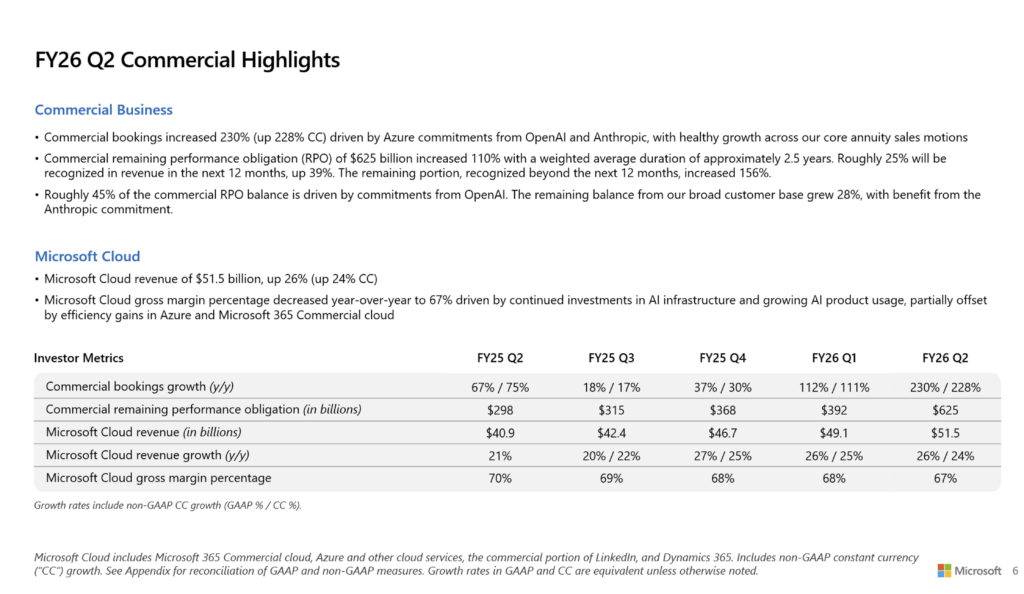

The quarter’s cloud momentum showed up in bookings and backlog indicators highlighted in Microsoft’s investor slides. Commercial bookings increased 230% (228% constant currency), which Microsoft attributed to Azure commitments from OpenAI and Anthropic. Commercial remaining performance obligation (RPO) increased 110% to $625 billion, and Microsoft said roughly 45% of the commercial RPO balance is driven by OpenAI commitments.

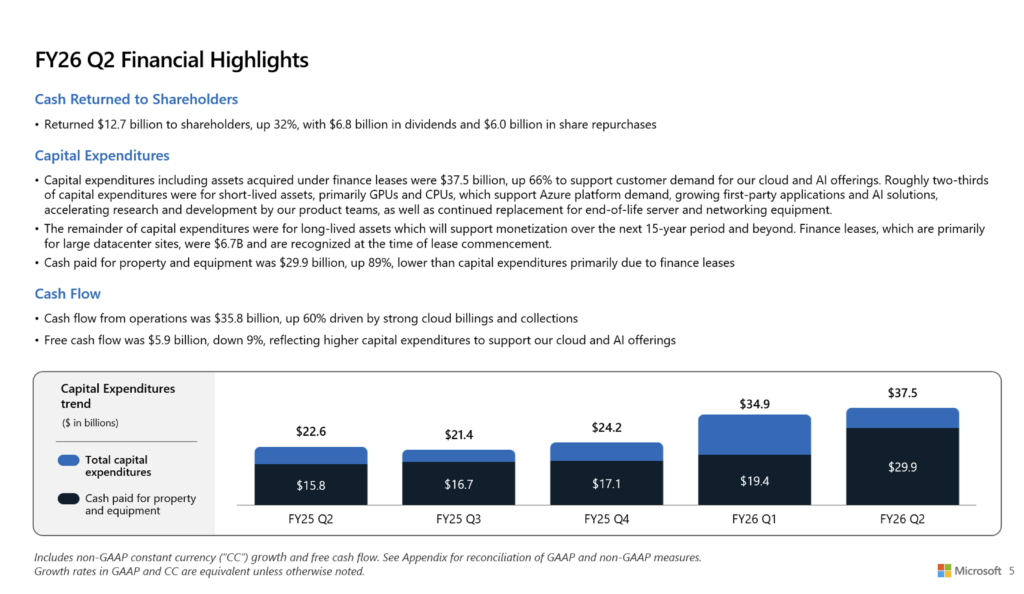

Microsoft’s AI infrastructure buildout continued to reshape capital intensity and margins. In its FY26 Q2 slides, Microsoft reported total capital expenditures (including assets acquired under finance leases) of $37.5 billion, up 66%, with roughly two-thirds going to short-lived assets such as GPUs and CPUs; it also cited $6.7 billion of finance leases primarily for large datacenter sites. Microsoft Cloud gross margin percentage declined to 67% year over year, which the company linked to continued investments in AI infrastructure and higher AI product usage, while cash flow from operations reached $35.8 billion and free cash flow was $5.9 billion (down 9%) due to higher capex.

- Q2 FY26 financial snapshot: revenue $81.3B (+17%); operating income $38.3B (+21%); GAAP net income $38.5B (+60%); GAAP EPS $5.16 (+60%); non-GAAP net income $30.9B (+23%); non-GAAP EPS $4.14 (+24%).

- Cloud growth: Microsoft Cloud revenue $51.5B (+26%); Intelligent Cloud revenue $32.9B (+29%); Azure and other cloud services +39% (+38% constant currency).

- Backlog and commitments (from slides): commercial bookings +230% (+228% constant currency); commercial RPO $625B (+110%); Microsoft said ~45% of commercial RPO is driven by OpenAI commitments.

- Data center capex (from slides): total capex incl. finance leases $37.5B (+66%); ~two-thirds for short-lived assets (GPUs/CPUs); finance leases primarily for large datacenter sites were $6.7B recognized at lease commencement; cash paid for property & equipment $29.9B (+89%).

- Margin signal: Microsoft Cloud gross margin percentage was 67% (down YoY), which Microsoft attributed to AI infrastructure investment and growing AI product usage, partially offset by efficiency gains.

- Shareholder returns: $12.7B returned in Q2 via dividends ($6.8B) and share repurchases ($6.0B).

“We are only at the beginning phases of AI diffusion and already Microsoft has built an AI business that is larger than some of our biggest franchises,” said Satya Nadella, chairman and chief executive officer of Microsoft.

Investor call takeaways

- Capex-to-revenue framing (ROI lens)

- Microsoft pushed back on mapping capex directly to Azure growth, arguing much GPU capacity supports first-party products (M365 Copilot, GitHub Copilot, Security/Dragon Copilot) plus internal R&D compute.

- CFO said if newly delivered GPUs from Q1–Q2 were allocated entirely to Azure, the Azure KPI would have been “over 40,” implying reported Azure growth reflects constrained allocation rather than demand limits.

- Management positioned optimization around “LTV portfolio” across multiple AI businesses while supply remains constrained.

- Hardware life, contracting, and margin durability

- CFO said many GPU purchases are “already contracted for most of their useful life,” and for large GPU contracts, “sold for the entire useful life of the GPU,” aiming to reduce lifecycle monetization risk.

- CEO added Microsoft uses software to continue running newer models on aging fleet, supporting smoother fleet “aging” rather than one-time gear spikes.

- CFO noted margins tend to improve over time as operational efficiency increases across an asset’s useful life (drawing analogy to CPU fleet behavior).

- Data center architecture and utilization focus

- Microsoft described the key optimization metric as “tokens per watt per dollar,” emphasizing utilization and TCO reduction via silicon, systems, and software.

- It cited a “50% increase in throughput” on a high-volume OpenAI inferencing workload used to power copilots.

- It described “Fairwater” data centers using a two-story design and liquid cooling to support higher GPU densities, plus an “AI WAN” linking Atlanta and Wisconsin sites into what it called an “AI super factory.”

- Capacity expansion cadence and geography

- Management said it added nearly 1 GW of total capacity in the quarter.

- CFO advised investors not to anchor on specific sites (e.g., Atlanta/Wisconsin) because they are multi-year builds; instead, focus on global capacity additions aligned to demand.

- Microsoft said it announced data center investments in seven countries in the quarter to address sovereignty and local data residency needs.

- Silicon strategy: vertical integration + multi-vendor flexibility

- CEO positioned Maia 200 results as workload-driven co-innovation (model + silicon + system), including rack-scale networking and memory optimization for inference.

- Microsoft emphasized it will not lock into one supplier: it highlighted NVIDIA and AMD alongside its own Maia accelerators and Cobalt CPUs, with the goal of best fleet-level TCO across generations.

- Maia 200: Microsoft said it delivers “10+ petaflops at FP4” and “30% improved TCO” vs the latest generation hardware in its fleet; it plans to scale initially for inference and synthetic data generation, plus Copilot and Foundry inference.

- “AI workloads need CPUs too” (implication for infra mix)

- CEO emphasized agents and tool use often spawn containers and workflows that run on general compute and storage, not only GPUs.

- Management linked ongoing cloud migrations (e.g., SQL Server IaaS momentum) to the need to provision balanced regional infrastructure (compute, storage, networking) alongside AI accelerators.

🌐 Analysis: Microsoft’s capex mix—heavy on GPUs/CPUs plus growing use of finance leases for large datacenter sites—underscores how hyperscalers are treating AI capacity as both a supply-chain challenge and a balance-sheet strategy. The Azure commitments tied to OpenAI and Anthropic also point to a market where long-term capacity reservations increasingly influence cloud growth and infrastructure planning alongside AWS and Google.