Intel’s Q3 2024 results, while reflecting challenges in profitability, underscore the company’s commitment to realigning its cost structure and innovating its product line. Revenue reached $13.3 billion, representing a 6% decline from the previous year, impacted by restructuring and substantial non-cash impairment charges related to Intel’s manufacturing assets. GAAP EPS fell to $(3.88) due to a $15.9 billion impairment charge and $2.8 billion in restructuring costs. However, Intel’s non-GAAP EPS was $(0.46), showing some resilience amid cost restructuring efforts.

CEO Pat Gelsinger highlighted Intel’s progress in streamlining operations, noting ongoing actions aimed at achieving $10 billion in annual cost savings by 2025. Intel’s Q3 also saw continued interest in its x86 and Intel 18A technology, suggesting future potential in the foundry space. Meanwhile, Intel has set guidance for Q4, estimating revenue between $13.3 billion and $14.3 billion, with a projected GAAP EPS of $(0.24) and non-GAAP EPS of $0.12, reflecting cautious optimism as it tackles cost issues.

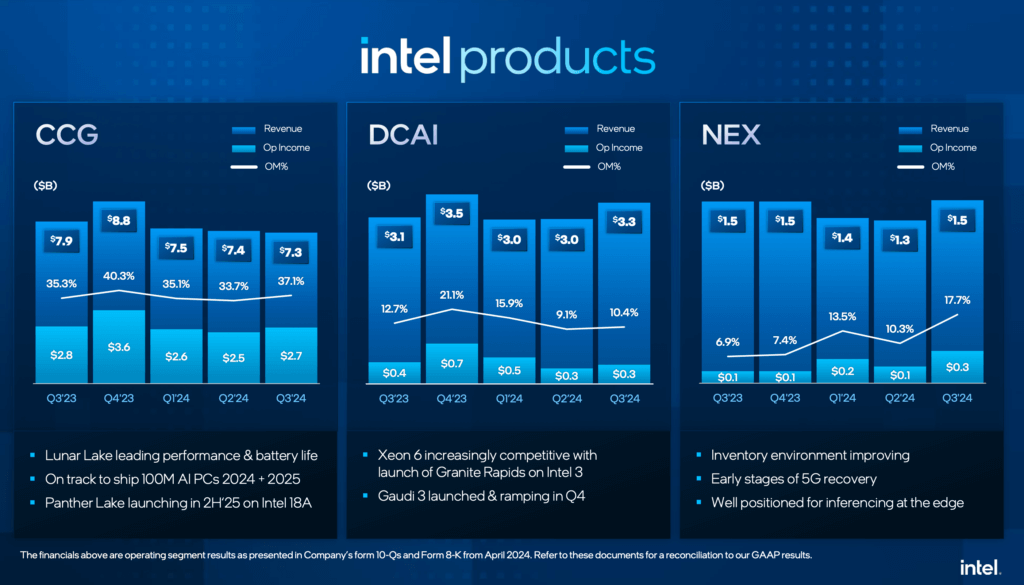

Intel also emphasized advancements across business units, notably in the Client Computing Group (CCG), Data Center and AI (DCAI), and Network and Edge (NEX). Collaboration with key partners like AMD and AWS signifies Intel’s strategic pivot towards collaborative tech innovation. Intel’s structural realignment, including a move to establish Intel Foundry as an independent subsidiary, aims to enhance operational focus and potentially pave the way for new funding opportunities.

Key Operational Metrics & Business Trends:

• Financial Highlights:

• Revenue: $13.3 billion (down 6% YoY)

• GAAP EPS: $(3.88); Non-GAAP EPS: $(0.46)

• Operating cash flow: $4.1 billion; Dividends paid: $0.5 billion

• Restructuring & Impairment Charges:

• Total impairment and restructuring: $15.9 billion in Q3 2024

• Restructuring costs: $2.8 billion aimed at workforce reduction and operational efficiency

• Segment Revenue Performance (YoY Changes):

• Client Computing Group (CCG): $7.3 billion, down 7%

• Data Center and AI (DCAI): $3.3 billion, up 9%

• Network and Edge (NEX): $1.5 billion, up 4%

• Intel Foundry: $4.4 billion, down 8%

• Mobileye: $485 million, down 8%

• Technology Developments:

• Intel 18A node advances; key partnerships with AWS and IBM

• Launch of Intel Core Ultra series for AI PCs, aiming to ship 100 million AI PCs by 2025

• Intel’s Gaudi 3 AI accelerators deployed in IBM Cloud, targeting large language models

“Our Q3 results underscore the solid progress we are making against the plan we outlined last quarter to reduce costs, simplify our portfolio and improve organizational efficiency. We delivered revenue above the midpoint of our guidance, and are acting with urgency to position the business for sustainable value creation moving forward,” said Pat Gelsinger, Intel CEO. “The momentum we are building across our product portfolio to maximize the value of our x86 franchise, combined with the strong interest Intel 18A is attracting from foundry customers, reflects the impact of our actions and the opportunities ahead.”

“Restructuring charges meaningfully impacted Q3 profitability as we took important steps toward our cost reduction goal,” said David Zinsner, Intel CFO. “The actions we took this quarter position us for improved profitability and enhanced liquidity as we continue to execute our strategy. We are encouraged by improved underlying trends, reflected in our Q4 guidance.”